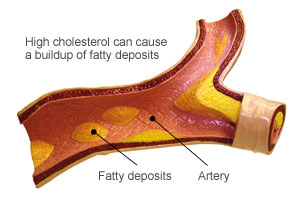

Cholesterol is a thing wax-like matter which is in every cell of the human body. Cholesterol is essential in the human body as it builds up the membranes in each cell. It’s an integral part in the production of hormones in our body, everyone has cholesterol.

On average, men in Ireland have a cholesterol level of 5mmol/L and women have a level of 5.1mmol/L. Our advice is you should see a doctor about your cholesterol if you’re over the age of 25. If you find you have high cholesterol and you’re looking to concentrate on bringing down your levels you should check out this PDF from the Irish Heart Foundation here – Link

This PDF will give you advice on how to treat high cholesterol by exercising regularly and will also outline what food groups should be eaten in the treatment of High Cholesterol. Some foods contain bad cholesterol and some contain good cholesterol. Make sure you understand what food can help.

Why would Cholesterol be considered in my life insurance application?

There are many reasons why cholesterol may be looked at while applying for life insurance but the main reason is to identify whether you are at risk of heart disease. This is why your insurance company may look ask the following questions –

• Do you have a history of heart disease or diabetes in your family?

• Have you ever needed treatment for cholesterol in the past?

• Do you smoke? (smoking can affect cholesterol as well.

• Are you overweight for your height and size?

• Are you overweight?

• Is your blood pressure raised?

So will High Cholesterol effect my premium?

The simple answer is yes. Life insurance is there to help the loved ones financially if you pass away. If an illness such as high cholesterol effects your heart, which it does, then you are less likely to live as long in life therefore you are a greater risk to the insurer.

If you truly want a better premium on your life insurance then our advice is seek medical advice and get to a healthier cholesterol level before you get your life insurance premium. Once you’ve done this, get your medical cert outlining your current health and you’re most likely to get a better premium.

Are you happy with your health?

If you’re happy and consider yourself a healthy person your next step is to seek advice and you could possibly get a cheaper policy. This is just my view on it. You’d really need to speak to a financial advisor before you go with a policy.